Abstract

Inflation targeting has been introduced as one of the monetary policy framework since the end of the 1990s. Forecasting inflation under the inflation-targeting monetary policy framework is also expected to improve with superior performance by constantly feeding updated information into the forecasting process, considering the domestic and global market conditions and developments. Literature evidence that inflation forecasting under inflation targeting is a challenging task with risk and uncertainty that are not easy to capture even in the latest modeling techniques. Inflation-targeting monetary policy was adopted by the Central Bank of Sri Lanka after the enactment of the Central Bank of Sri Lanka Act with effect from 15.09.2023. This study examines inflation forecasting under the inflation-targeting monetary policy in Sri Lanka implemented with a clear mandate assigned in the agreement for a flexible inflation targeting framework to guide the market and inflation expectations. Automatic ARIMA forecasting techniques are employed to forecast inflation using two series of price indices with different base years from 2016M01 to 2026M12, and 2022M01 to 2026 M12 including 30 months as forecasting length. According to the findings, inflation forecasting is in line with the 5 percent targeted level with a 3 percent margin to fluctuate for both sides subject to the upside and downside risk factors. Accordingly, Inflation forecasting is within the inflation projections indicated under the inflation fan chart. It further suggests that inflation has been gradually stable in SL compared to the recently elevated inflation experience. Therefore, inflation targeting and projections can be used to shape and guide market expectations to facilitate decision-making in forward looking policies toward achieving and maintaining domestic price stability, which is the primary objective of the Central Bank of Sri Lanka.

Keywords

Inflation Targeting, ARIMA, Inflation Fan Chart, 5% Targeted Level, CBSL

1. Introduction

Forecasting is vital in decision-making, shaping expectations while living in the present and thinking and dreaming about the future with uncertainty. Inflation forecasting refers to the technical analysis and estimation process for predicting inflation rate with forward-looking, shaping price expectations to facilitate better decision-making, and formulating macroeconomic and other policies subject to the risk and uncertainty level. Inflation can be defined as the rate of change in the price level of a country that is measured using price indices. Inflation has been identified as the

“number one public enemy for an economy” unless necessary demand-side policy measures have not managed it

| [1] | Batten, Dallas S. "Inflation: The cost-push myth." Federal Reserve Bank of St. Louis Review 63.6 (1981): 20-26. |

[1]

. Anyway, we have learned about the advantage of inflation for an economy, which is the major encouraging factor in enhancing business activities with well-managed lower fluctuation levels to improve economic activity towards the potential level of GDP. In monetarism, inflation is identified as

“inflation is always and everywhere a monetary phenomenon”, elaborating the demand side, and significant impact on inflation other than cost-push inflationary factors

. Inflation forecasting techniques are being developed to estimate the most possible figure under different scenarios to guide the market and expectations in forward looking policies. Monetary authorities adopt different frameworks in conducting monetary policy depending on the macroeconomic development level and international practices. Policy regimes, in conducting monetary policy have been changing from exchange rate regimes, monetary targeting regimes towards inflation targeting framework by advanced and emerging economies. Further, under the inflation targeting monetary policy framework, inflation forecasting is a crucial feature to guide the market and inflation expectation for the countries. Therefore, accurate inflation forecasting is of utmost importance for policymakers, businesses, investors, and other agents for navigating the economy to a better forward position.

Four essential requirements are discussed (IMF, 2002) to ensure successful implementation of monetary policy under the inflation targeting framework

| [3] | Carare, Alina, et al. "Establishing initial conditions in support of inflation targeting." (2002). |

[3]

. The paper describes four initial requirements. 1. Mandate supporting inflation targeting and accountability for achieving the objective. 2. Macroeconomic stability of the country. 3. Financial system stability and development. 4. Effective policy implementation tools for establishing a well-equipped research unit with inflation forecasting techniques are emphasized and recommended for countries that have adopted inflation-targeting frameworks in conducting monetary policy. Anyway, in this article, it is evident that countries have adopted inflation-targeting frameworks by adhering to several requirements rather than all requirements mentioned, subject to the availability of a conducive legal and financial environment reflected under the essential requirements. Literature evident that New Zealand as the first country to adopt a inflation targeting monetary policy framework in 1998. Many developed countries adopted the framework while developing countries adopted it after ensuring the availability of the required conditions. As a result of a long study about the feasibility of adopting a new framework, the Central Bank of Sri Lanka (CBSL) also adopted inflation targeting framework for conducting monetary policy with the enactment of the Central Bank of Sri Lanka Act (CBA) No. 16 of 2023 with effect from 15.09.2023 pursuing two objectives of which the primary aim of achieving and maintaining the domestic price stability

| [4] | Central Bank of Sri Lanka Act (CBA) No. 16 of 2023. |

[4]

. CBSL conducts monetary policy under the inflation-targeting framework to achieve and maintain domestic price stability. Further, an agreement has been signed with the Government in setting the inflation target as 5 percent for the next 2-3-year period with a 2 percent flexibility to up and down margins, allowing to move with a certain level of probability as visualized in inflation Fan chart, a key feature under the inflation targeting monetary policy framework. Among the other key features of monetary policy tools under the new framework, monetary policy communications have been identified as an effective policy tool to make aware the market on the policy decisions and reactions, shaping inflation expectations to facilitate a better decision-making process to achieve short-term and medium-term macroeconomic targets including economic growth and distributions of resources effectively. The monetary policy report, a new report under the provision of CBA, is published covering the monetary policy decisions, the rationale for arriving at the decisions, and guiding the market by providing inflation and economic growth forecasting with a medium-term outlook. Further, under the initial requirement, establishing a forecasting unit is vital in facilitating data-base updated forecasting information to guide the market in regularly shaping inflation expectations toward a futuristic outlook. Adopting inflation targeting reflects the independence of the central bank operations with more accountability in its policies to the parliament and the public, ultimately improving the credibility of the central bank policies.

Under the theoretical and empirical literature, the desirable level of inflation for developed and developing countries has been identified. Accordingly, maintaining 2 percent or below 2 percent inflation for developed economies and 5 percent or above level inflation for other countries has been recommended as the desired level of inflation. However, single-digit and mid-single inflation are among the popular wording that comes across under the desired level of inflation for a country. Despite the desired and target inflation level, we have evidence that higher inflation, hyperinflation, disinflation, deflation, and stagflation have been experienced by both developed and developing countries, reflecting macroeconomic imbalances resulting from policy measures implemented, causing shocks in demand-pull, cost-push, or inflation expectations.

As per inflation targeting and financial stability, Heise M, 2019 explains with countrywide evidence that countries have adopted Inflation targeting monetary policy framework before the Great Financial Crisis (GFC) reported during 2007-2009

| [5] | Heise, Michael. Inflation Targeting and Financial Stability: Monetary Policy Challenges for the Future. Springer, 2019. |

[5]

. Accordingly, inflation targeting was the framework for monetary policy adopted by several countries during the great financial crisis. The final blame for the GFC was passed to the major central banks for their expansionary, ultra-expansionary monetary policy measures that had been implemented before the crisis and after the crisis as types of unconventional monetary policy measures that have evidence for less effectiveness in stimulating economic growth and activities. Therefore, the inflation targeting framework was already challenged during the great financial crisis. Heise recommends to consider financial stability in conducting monetary policy in addition to inflation targeting to delay possible crises that could emerge in the future. Financial stability also has been pointed out as an initial requirement for implementing inflation targeting too. Further, in the decision-making regarding risk and uncertainty, Heise pointed out that financial markets, equipment, techniques, and modeling can capture all possible risks other than the uncertainty that may occur from political influence on the economy. Therefore, while developing sophisticated different modules of forecasting to guide the market, the impact from the fiscal side and political authority of the country also to be considered. In this context, Inflation targeting is a challenging but popularizing framework; it is still being used by major central banks and other economies, considering “inflation as the Number one enemy for an economy” until the relevant authorities establish the another new framework for monetary policy implementation.

Theoretical and empirical researches are well established for inflation, the primary macroeconomic variable under mainstream economics. Empirical literature covering the countries adopted to inflation targeting and forecasting is also available since inflation targeting has been adopting since 1998 with the essential requirement for well-established research and forecasting unit for the monetary authority to guide the market expectation and to facilitate forward-looking policies by promising that central bank would keep the inflation at a targeted level to stimuli economic activities. Since Sri Lanka has recently adopted the inflation targeting framework, the empirical literature is hardly available, with inflation forecasting supported by the targeted level of 5 percent inflation with 2 percent flexible margin. Therefore, this study aims to provide the necessary literature on inflation forecasting by adopting an appropriate methodology depending on the results of the diagnostic tests performed for the data covering the sample periods. Therefore, filling the existing literature gap on inflation forecasting under the inflation targeting framework and develop the literature is the objective of this study. Further, inflation forecasting using recently published data under CCPI 2021=100 is employed limiting to a sample from 2022 onwards and therefore, as an alternative approach, another model using data series of CCPI 2013=100 is estimated to better analyse the results with sample size over 100 observations. Accordingly, null hypothesis of H0: inflation forecasting is not in line with the inflation targeting framework established is rejected indicating the inflation forecasting in this paper is in line with the inflation targeting framework and therefore can be used for policy level recommendations and other inferences. The empirical literature is reviewed in section two, methodology in section three and the inflation targeting framework in Sri Lanka will be discussed in section four. The results of the inflation forecasting module will be interpreted in section five. Finally, conclusion is made with the recommendations based on the model estimated in the last section of the paper.

2. Literature Review

In this section, the empirical literature on the impact of inflation on macroeconomic variables, inflation forecasting modules, and recently developed inflation forecasting module under the inflation targeting framework in conducting monetary policy is expected to be reviewed to improve the understanding of the relationship with other macroeconomic variables, and inflation forecasting modules that based on the various estimation techniques. Further, the relationship between inflation and economic growth and its impact on other selected variables are discussed to identify the overarching effect of inflation on the householder decision-making process and the economy. Inflation targeting and its impact on macroeconomic variables are expected to be reviewed, subject to recent evidence in the literature and the methodology adopted, using different techniques under time series data analysis. Therefore, the literature will be reviewed concerning empirical and methodological aspects available in published articles covering advanced and emerging market economies. A conclusion is made justifying the requirement for the study on the inflation forecasting model under inflation-targeting monetary policy to fill the gaps in the empirical literature.

Understanding the relationship between inflation and other macroeconomic variables is paramount in identifying the economic impact. As per the theory, inflation has been introduced to replace one variable of the traditional Phillip curve relationship built using unemployment and wage rates. Accordingly, the new Phillip curve was developed to describe the relationship between unemployment and inflation instead of the wage rate assuming the wage rate also represents in the inflation rate. Accordingly, the theory of the inverse relationship between inflation and unemployment was established based on the country’s experience capturing an extended period. Unemployment is also a macroeconomic variable related to an economy’s medium- and long-term activity. With the development of the importance of pricing and pricing mechanisms to signal the economy, inflation has been widely using popular macroeconomic variables in describing short-term relationships under the popular wording of Monetarism: “Inflation everywhere is a monetary phenomenon”

| [6] | Mishkin, Frederic S. "The causes of inflation." (1984). |

[6]

. Accordingly, Interest rate and inflation are positively related. In contrast, interest rate and inflation rate while economic growth is assumed to have a negative relationship, indicating a higher inflation rate and interest rate with lower economic growth or economic contraction in worst case scenario.

Literature about demand side factors that impact inflation is more popular than the supply side factors. As per the evidence of Riswan on Determinants of inflation, monetary and macroeconomic perspectives, discussing the impact of demand entire factors, money circulating in the economy on inflation in the form of money in the transactions for export, imports, and money under the saving and several monetary factors that affect inflation as findings, by employing a regression analysis using secondary sourced data

| [7] | Ridwan, Muhammad. "Determinants of Inflation: Monetary and Macroeconomic Perspectives." KINERJA: Jurnal Manajemen Organisasi dan Industri 1.1 (2022): 1-10. |

[7]

. Further, it suggests that financial and economic factors on the supply side have the most impact on inflation and other supply-side factors.

Cioran Zina investigated to find the about Monetary Policy, Inflation, and the Causal Relationship between the Inflation Rate and Some of the Macroeconomic Variables such as inflation and interest rate, inflation and unemployment using regression analysis

| [8] | Cioran, Zîna. "Monetary policy, inflation and the causal relation between the inflation rate and some of the macroeconomic variables." Procedia Economics and Finance 16 (2014): 391-401. |

[8]

. The study concludes a significant inverse relationship between inflation and the unemployment rate, indicating that the inflation rate is an effective instrument in managing an economy’s unemployment rate for the data 1990-2013 under the Euro region countries by following a simple analysis. Also, it finds a strong positive relationship between monetary policy interest rate and inflation while emphasizing the requirement of crucial attention on commitment, consistency, dynamics, transparency, accountability, quality assessment, and avoidance of excessive fluctuation and flexibility in implementing monetary policy. According to the findings, more responsibility has been given to the relationship between economic policy rate and inflation to examine the impact on macroeconomic variables, which identify as variables that are related to the medium and long term.

Energy price impact of inflation is also a widely used topic to discuss risk factors for significant price volatility. Alessandro Cologni a, Matteo Manera b studied Oil prices, inflation, and interest rates in a structural cointegrated VAR model for the G-7 countries and made several conclusions among them, ii) according to the estimated coefficients of the structural part of the model, for all countries except Japan and U. K. the null hypothesis of an influence of oil prices on the inflation rate cannot be rejected implying that inflation is not affected from oil price during the period

| [9] | Cologni, Alessandro, and Matteo Manera. "Oil prices, inflation and interest rates in a structural cointegrated VAR model for the G-7 countries." Energy economics 30.3 (2008): 856-888. |

[9]

. Further, it shows that inflation rate shocks are transmitted to the real economy by increasing interest rates. Akdeniz İİBF Dergisi 2019 studied the impact of import volume on the domestic inflation rate in the Turkish economy for the period 1961-2017 by utilizing a proper cointegration technique

| [10] | Tuğcu, Can Tansel, Ayşe Meral Uzun, and İlyas Özkök. "The impact of import on inflation: An ARDL analysis for the Turkish economy." Akdeniz İİBF Dergisi 19. 2 (2019): 415-426. |

[10]

. Findings indicate that monetary impact and imports are the primary reasons for inflation. Therefore, policymakers should consider this bilateral structure when dealing with general price level instabilities in the Turkish economy. Another study investigating the impact of oil prices on macroeconomic variables by way, Akin was conducted, considering great attention to the impact of oil prices on the macroeconomic variables of an oil exporter in Nigeria

| [11] | Iwayemi, Akin, and Babajide Fowowe. "Impact of oil price shocks on selected macroeconomic variables in Nigeria." Energy policy 39.2 (2011): 603-612. |

[11]

. The finding shows that oil price shocks do not majorly impact macroeconomic variables in Nigeria, while adverse oil price shocks significantly impact output and exchange rate. Further the study investigated the impact of oil price change on inflation, Man, Yen examines the impact of oil prices on inflation, interest rates, and money using different lag lengths with impulse responses

| [12] | Wu, Man-Hwa, and Yen-Sen Ni. "The effects of oil prices on inflation, interest rates and money." Energy 36.7 (2011): 4158-4164. |

[12]

. Findings imply that monetary policies still matter after accounting for the oil prices and the energetic variable, with the above robustness concerns.

AO Adaramola, O Dada examine the influence of inflation on the economic growth of Nigeria by employing an autoregressive distribution lag module for the variables considered GDP, Inflation rate, Interest rate, exchange rate, degree of openness of the economy, money supply and govt expenditure on consumption for the period from 1980-2018

| [13] | Adaramola, Anthony Olugbenga, and Oluwabunmi Dada. "Impact of inflation on economic growth: evidence from Nigeria." Investment Management & Financial Innovations 17.2 (2020): 1. |

[13]

. According to the findings, inflation and exchange rate negatively impact economic growth, while interest rate and money supply positively impact economic growth. As per the unidirectional relationship investigated, there is no unidirectional relationship between inflation and the degree of openness of the economy. In contrast, unidirectional relationships existed between other variables. Considering the positive relationship between money supply and economic growth during the period, the study recommends a more pragmatic monetary policy to target inflation and stimulate economic activities. Damayanti et al investigate the influence of macroeconomic variables on inflation in Indonesia using a VECM model for 1989-2019 with cointegrated data detected at diagnostic tests. It concludes that inflation positively responds to interest rates and money supply, implying that inflation is sensitive to the macroeconomic variable in Indonesia

| [14] | Damayanti, Sekar Ayu, and Gentur Jalunggono. "Analysis Of The Influence Of Macroeconomic Variables On Inflation: The Vecm Approach." JOURNAL OF HUMANITIES, SOCIAL SCIENCES AND BUSINESS 2.1 (2022): 199-218. |

[14]

. Kryeziu et al. Durguti examine the impact of inflation on economic growth in Eurozone countries from 1997 to 2017 using multiple linear regression modules and the VAR module. Results indicate that inflation is positively impacting economic growth for the Euro Area

| [15] | Kryeziu, Nexhat, and Esat Ali Durguti. "The impact of inflation on economic growth: The case of Eurozone." International Journal of Finance & Banking Studies (2147-4486) 8.1 (2019): 01-09. |

[15]

. The results reflect that comparably lower inflation levels exist in Eurozone countries; lower inflation encourages economic activities based on a desirable level of 2 percent inflation for developed countries. Hoang et al. study the impact of macroeconomic factors on inflation, considering the escalating inflation from 2008 with the effect of the 2008 Great Financial Crisis. The VAR model examines the impact of macroeconomic variables, including money supply, credit growth, exchange rate, GDP, and inflation

| [16] | Hoang, T., and V. Thi. "The impact of macroeconomic factors on the inflation in Vietnam." Management Science Letters 10.2 (2020): 333-342. |

[16]

. The findings indicate that the government and the State Bank must maintain their inflation control objectives to contribute to macroeconomic stability, support rational growth, and ensure social security.

Among the empirical literature available under inflation targeting, Zherlitsyn, Dmytro investigate the impact of inflation targeting on macro-economic indicators using data from 2011-2019 in Ukraine during the period of stability and crisis by employing a multivariate regression and simultaneous equation model

| [17] | Zherlitsyn, Dmytro. "The impact of inflation targeting on macroeconomic indicators in Ukraine." Mykhailo Kuzheliev, Dmytro Zherlitsyn, Ihor Rekunenko, Alina Nechyporenko and Figuram Nemsadze (2020). Banks and Bank Systems 15.2 (2020): 94-104. |

[17]

. According to the findings, inflation does not affect fundamental economic indicators. Further, a significant impact has been observed between inflation and unemployment, spending on consumption, exchange rate, and monetary policy instruments. Another study on inflation targeting monetary policy, Macroeconomic performance of inflation targeting in European and Asian emerging economies, is examined Milojko et al. this study covers 26 emerging market economies in Europe and Asia region for the period from 1997-2019 and the focused period from 2008-2019 employing two approaches, dynamic panel modeling, and propensity score matching framework

| [18] | Arsić, Milojko, Zorica Mladenović, and Aleksandra Nojković. "Macroeconomic performance of inflation targeting in European and Asian emerging economies." Journal of Policy Modeling 44.3 (2022): 675-700. |

[18]

. Findings suggest that inflation targeting effectively reduces inflation rate, volatility, and GDP volatility. According to the econometric model results, inflation targeting has not affected economic growth. The findings suggest that inflation targeting improves the macroeconomic performance of developing countries even if they partially fulfill the standard requirements for its implementation.

Literature covering the East Asian countries that adopted inflation target framework has been examined by Valera et al. covering four East Asian emerging market economies, Indonesia, Korea, Philippines, and Thailand, while Malaysia also has included a country that has not been adopted to Inflation targeting

| [19] | Valera, Harold Glenn A. Inflation and Macroeconomic Effects of Inflation Targeting in Asia: Time-Series and Cross-Country Analysis. Diss. University of Waikato, 2017. |

[19]

. Different findings for each country can be given that Korea shows inflation targeting adopted and evidencing inflation responsive and forward-looking policy stance to achieve price stability. Other countries have conducted inflation-targeting monetary policy with a backward-looking policy stance, and the Philippines and Malaysia have inflation-targeting monetary policies. The Philippines and Malaysia are not inflation-responsive policy impact compared to other countries. Evidence from emerging market economies on inflation targeting and economic performance has been examined Duong et al. using a balanced panel data of 54 countries, of which 15 were inflation-targeting countries from 2002 to 2010

| [20] | Duong, Thuy Hang. "Inflation targeting and economic performance over the crisis: evidence from emerging market economies." Asian Journal of Economics and Banking 6.3 (2022): 337-352. |

[20]

. According to the findings, there is no significant difference between the inflation rate and GDP growth in both categories of countries during the period. However, the finding suggests that inflation increases in emerging economies can be controlled when the economy has to cope with exogenous uncertainties. Further, the inflation targeting framework helps emerging market economies manage inflation during the crisis.

Forecasting inflation has been an essential component of inflation-targeting monetary policy. Özkan et al. et al. Yazgan investigating whether forecasting inflation is easier under a targeting monetary policy framework; the answer is no. It will not be more accessible to forecast inflation with a given level of upside, downside risk, and uncertainties to guide the market expectation

| [21] | Özkan, Harun, and M. Ege Yazgan. "Is forecasting inflation easier under inflation targeting?." Empirical Economics 48 (2015): 609-626. |

[21]

. The findings indicate that forecasting performance is generally superior under IT compared to non-IT framework. Therefore, the accuracy of inflation forecasting is higher under the inflation-targeting monetary policy framework.

Regarding inflation targeting and model-based forecasts, a study by Levin examines the role of the model-based forecast in the monetary policy process in the UK

| [22] | Levin, Andrew, Volker Wieland, and John C. Williams. "The performance of forecast-based monetary policy rules under model uncertainty." American Economic Review 93.3 (2003): 622-645. |

[22]

. The study refers to the quarterly basis model updates, continuous research, and statistical approaches. According to the study, in addition to the model being based on a consistent framework, alternative scenarios, and risk, the importance of judgment on risk and uncertainty also has been identified as having a significant role in constructing inflation forecasts under inflation targeting. With these, a forecast-centered approach for inflation targeting is passed among several to illustrate the wide range of uncertainties in central projections. The asymmetric behavior of inflation is explored by Akdoğan, Kurmaş under inflation targeting. It discussed the asymmetric policy response of the central bank around the inflation target and asymmetric inflation persistence

| [23] | Akdoğan, Kurmaş. "Asymmetric behaviour of inflation around the target in inflation‐targeting countries." Scottish Journal of Political Economy 62.5 (2015): 486-504. |

[23]

. The paper suggests an Asymmetric Exponential Smooth Transition Autoregressive (AESTAR) model to capture the asymmetric movement of inflation, and the model is justified with high predictive power compared with an out-of-sample forecasting exercise.

Inflation targeting and financial stability Woodford examine after the GFC, the severity and risk to financial stability have increased due to extra expansionary monetary policy measures

| [24] | Woodford, Michael. Inflation targeting and financial stability. No. w17967. National Bureau of Economic Research, 2012. |

[24]

. therefore, the central bank should reconsider financial stability too in setting targets for monetary policy due to shocks and fluctuations in monetary policy decisions are absorbed into the financial sector and record lower performance, lower effectiveness of monetary policy transmission mechanism and distributional channels in achieving medium- and long-term objectives of an economy. The finding suggests setting a target for financial stability despite possible risk, volatility, and financial crisis issues. A similar conclusion was made by Heise in this book on inflation targeting and financial stability

| [4] | Central Bank of Sri Lanka Act (CBA) No. 16 of 2023. |

[4]

.

Concluding to the literature reviewed above, the theoretical relationship between inflation and other macroeconomic variables is evidenced in most studies. Lower desired inflation in Euro countries had positively impacted economic growth during the period considered. The inflation and unemployment relationship could be observed as an antagonistic relationship that links inflation as a short-term and unemployment as a long-term variable. Accordingly, adopting an inflation-targeting framework and successfully achieving the objectives will reduce unemployment to a certain extent. However, Heise explains that the expected negative relationship between inflation and unemployment weakened during the great financial crisis after 2008, even with extra expansionary monetary policies with higher inflation and unemployment rates. Literature related to inflation targeting suggests that inflation targeting is helpful in improving the macroeconomic performance of developing countries even when they adopt inflation targeting by partially fulfilling the initial requirements. There is no evidence of success story for all economies that adopted inflation targeting, while several economies show lower inflation with the target. In contrast, the economy performed under lower eco-nomic growth. The book suggests that inflation targeting, and financial stability should be considered as a monetary policy framework after the global financial crisis to ensure the economy's stability. The financial sector was the most affected, with expansionary and ultra-expansionary policy approaches to unconventional monetary policy measures adopted in the Euro, USA, and Japan and for other different macroeconomic imbalances. A positive relationship between inflation, interest rates and key policy rates has been identified in the empirical literature. Therefore, this relationship could still effectively stimulate economic activities by adjusting the policy rates decided by the monetary policy committee, which is expected to be affected through monetary transmission channels. Several pieces of literature available after the global financial crisis conclude that monetary policy to be targeted both inflation and financial stability due to the financial sector being severely impacted by unconventional monetary policy measures and forward guidance policy measures adopted after 2008. The accuracy of the inflation forecasting model is expected to be superior, with the quarterly forecast constructed the inflation forecasting model is expected to be superior, with quarterly forecasts constructed on monthly update data published using the consumer price index. Single variable model analysis techniques have been employed to forecast inflation with different model specifications for cross-country and individual analysis using data with more frequency for recent studies. The empirical literature on the impact of inflation on macroeconomic variables, determinants of inflation, and the forecasting model for inflation are widely available, covering developed and emerging economies. Literature on Inflation forecasting under inflation targeting monetary policy framework is still growing. At the same time, some countries are still adopting flexible inflation targeting to guide the market in a forward-looking approach. A study of Rohini on Inflation forecasting using the Automatic ARIMA forecasting model in Sri Lanka has covered the period from 2016 to 2023 for the forecasting length of 2 years

| [25] | Liyanage, D. R. "Inflation forecasting using automatic ARIMA model in Sri Lanka." International Journal of Economic Behavior and Organization 11.2 (2023). |

[25]

. The finding reveals that single-digit inflation will remain with fluctuations for the forecasting period. Given the importance of inflation forecasting after adopting a flexible inflation targeting framework in Sri Lanka with the enactment of CBA after Q3 2023, this study aims to forecast inflation employing more data with improved sample sizes for two series CCPI 2013=100 and CCPI 2021=100 under the inflation targeting framework with a forward-looking approach. Recommendations will be made considering the findings of the inflation forecasting model for the relevant areas that would impact interest rates and other macroeconomic variables toward achieving medium-term objectives.

3. Methodology

Econometric forecasting techniques are expected to be employed to forecast inflation using the Colombo Consumer Price (CCPI) Index published by the Department of Census and Statistics (DCS). Monthly Secondary sourced data is employed for the study covering two series for different base years CCPI= 2013 and CCPI=2021, considering the forecasting comparison and accuracy supporting a long data series. Accordingly, the Colombo Consumer Price Index (CCPI) monthly data for the period spanning from 2016M01 to 2024M06, covering forecasting lengths up to 2026, 30 months, will be used for CCPI=2013 to forecast inflation. Sample for CCPI 2013=100, is considered from 2016 onward avoiding 2015 being an election year and with sufficient number of samples over 100 observations. Further, another forecasting module, using the same techniques for the CCPI=2021 monthly data series spanning from 2022M01 to 2024M06, is estimated to cover 30 months of the same forecasting length for headline inflation, which refers to the inflation, including all goods and services that are considered in the consumer basket of goods and services. A graph is developed using forecasted data combined with realized inflation, forecasting, and targeted level to facilitate inflation targeting, guide the market, and shape market expectations in line with a forward-looking policy approach. CCPI monthly data under two series are tested for diagnosing stationarity, ACF, and PACF and detecting autocorrelation and partial autocorrelation with AR and MA term specifications. Accordingly, the appropriate model will be selected with the support of EViews version 13.0, interpreted with forecast summary and comparison, further AIC and Bayesian Information criteria will be used to select the best model out of 25 models estimated.

The empirical literature is evident that forecasting for single variable module is supported by Autoregressive (AR) and Moving Average (MA), ARIMA modules that were introduced by Box, George EP

| [26] | Box, George EP, and David A. Pierce. "Distribution of residual autocorrelations in autoregressive-integrated moving average time series models." Journal of the American statistical Association 65.332 (1970): 1509-1526. |

[26]

. Accordingly, Autoregressive Integrated Moving Average (ARIMA) further improved the model considering integration of both as Auto Regressive Integrated Moving Average (ARIMA) modules subject to a given level of specifications for Maximum Differencing, AR term, MA term, and Seasonal components if any are widely using for single variable model forecasting purposes. Therefore, the expected model to estimate inflation forecasts for two series is given below.

Y=β1Y(t-1)+β2Y(t-2)+……+et-α1e(t-1)-α2e(t-2)(1)

Y: Targeted variable

β1, β2: Coefficient, the rate which indicates the impact on Y by a change in Y(t-1), Y(t-2)

Y(t-1), Y(t-2): Previous year/ month values of the variable

et: Error term

This module is estimated subject to conducting the diagnostic test to identify the stationary level of data, performing ACF and PACF to check the autocorrelation and partial autocorrelation, and determining the AR, MA term. After the model's goodness of estimating, the model's goodness of fit is tested with other options. Further, forecast comparison and average forecasting are to be done separately to interpret the results. Then, analytical software has also been developing techniques to facilitate estimation and forecasting using the same techniques with the more improved enhanced higher and maximum number of estimations, forecasting that may be difficult to estimate manually. Therefore, in this study, the Automatic ARIMA forecasting model is employed to forecast inflation using two series for different base years, which compatible the results with the criteria we determined using basic tests.

4. Inflation Targeting Monetary Policy Framework in SL

4.1. Inflation in Sri Lanka

Inflation can be identified as the rate of change in the price level of a country that is measured using price indices over a given period. Inflation has been a critical macroeconomic variable influencing market expectations and economic activities in the short term to achieve medium-term targets. Inflation targeting is adopted in conducting monetary policy as the framework under the provision of CBA to achieve the primary objective of the CBSL. Accordingly, inflation has been the target in the monetary policy framework. Inflation in Sri Lanka is measured using CCPI, has named as the official price index and measured from 1952 =100, revising base years in several times and published by DCS monthly. The base year revision for CCPI = 2021, has considered the enhanced expenditure pattern of consumer behavior, weightage of a basket of goods and services, and sample coverage. Movements of the Inflation in Sri Lanka can be observed under separate periods: moderate inflation, single-digit inflation, mid-single inflation, and elevated inflation, which could manage below 70 percent that we experienced recently and after that, lower inflation with a targeted level of 5 percent as per provision of inflation targeting mandate agreed with the government under the CBA.

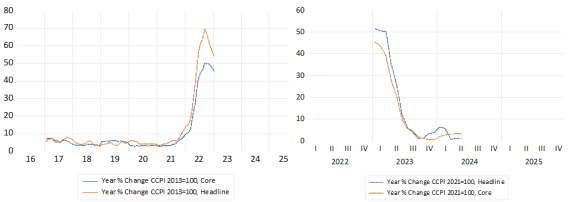

As in best practices, headline and core inflation data are published using secondary sources and official websites. The monthly press release informs the stakeholders, journalists, and public via media channels. Headline inflation covers the price of all goods and services in the consumer basket. Core inflation is measured by excluding selected items that lead to higher volatile prices under the food and energy category to indicate a clear reflection of medium- and long-term trends in inflation. Headline and core Inflation in Sri Lanka for the period measured by CCPI is shown below.

Figure 1. Inflation movements in Sri Lanka for (CCPI = 2013), (CCPI=2021), Headline and Core.

As per the above figure, during the period considered, inflation in Sri Lanka has moved below 10 percent except for the extremely high inflation recorded for a recent two-year period from 2021-2023, which reflects the instability of macroeconomic developments and external sector imbalances of the country. After this, with the enactment of CBA, a new framework called the inflation targeting framework was adopted in conducting monetary policy pursuing the primary objective; of achieving and maintaining domestic price stability. According to CCPI 2021 = 100, inflation in Sri Lanka is moving around 5 percent aligning with the targeted level.

4.2. Key Features of Inflation Targeting Framework

A new framework called inflation targeting was adopted to conduct monetary policy as per the provision of the CBA. Accordingly, a 5 percent inflation target has been set jointly with the government by signing an agreement specifying a clear mandate to achieve and maintain domestic price stability as the primary objective of the CBA. Further, a 2 percent up and down margin has been added to the targeted level of inflation to allow flexibility, considering the risk associated with moving away the inflation from the target level. Accordingly, under the Flexible Inflation Targeting (FIT), inflation in Sri Lanka may move within 3 –7 percent around the 5 percent targeted level. In case of a missed target for two consecutive quarters, the monetary authority should submit a report to Parliament through the Ministry of Finance explaining the reasons for deviating the inflation from the expected path. Further, this report is also to be made available to the public. Therefore, adopting inflation targeting monetary policy framework in Sri Lanka indicates the accountability of its policies to the Parliament and public.

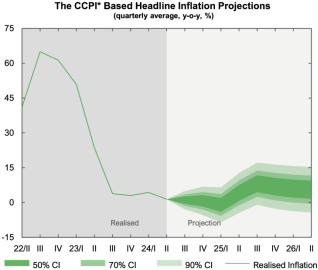

Guiding and shaping the market expectations by providing updated inflation forecasting information towards the next 2–3-year period, depicted in the inflation fan chart, is also a vital feature of the inflation targeting framework. The inflation fan chart can be identified as a combination of realized inflation with forecasted inflation for the future with a given probability level to indicate uncertainty and deviations from the target level of inflation. However, it must be noted that the inflation fan chart is a guide, not a promise while indicating further risk and uncertainty captured under the upside and downside risk of deviating inflation projections from the target level. The inflation fan chart used to guide the market in managing inflation expectations is shown below.

Figure 2. Inflation fan chart.

According to the inflation fan chart, the realized inflation shows from 2022 Q1 to 2024 Q2 while inflation projections guide the rest of the period, indicating the inflation within the 5 percent target level with volatility in the shaded area around that has done using available data, assumptions, and judgments considered at the recent monetary policy review cycle. Further, the forecast and inflation fan chart is updated with quarterly basis information, using monthly data on inflation updates and for inflation press releases, as well as in the monetary policy press releases. Moreover, forecasted inflation and realize, last updated inflation should be indicated in the fan chart to guide the inflation expectation with forward looking policies. Accordingly, it will be observed that the forecasted inflation is also in line with the realized inflation in the same trends with upward and downward movements. Therefore, if the estimated forecast is consistent with the actual realized inflation, the inflation fan chart can be used as a guide to shape the market expectation and to manage inflation expectation, thereby reducing the error of the inflation expectation survey, which ultimately helps to improve the inflation forecast visualized in the fan chart.

A new report named as monetary policy report is published as indicated in the advanced released calendar posted on the official website. The monetary policy report describes the rationale for the monetary policy decisions, considering the economic outlook, macroeconomic developments, and recent trends in the global economy, and other important factors, if any. Further content of the monetary policy report includes the forecast for the medium-term outlook, which covers the inflation forecast and forecast for economic growth. Therefore, this medium-term forecast of inflation and economic growth indicates the country’s macroeconomic outlook, which further helps guide the market to facilitate better decision-making and shaping expectations.

In addition, monetary policy communication has also been identified as an important policy tool under the inflation-targeting framework. Immediately after the monetary policy report is published, panel discussions and briefing sessions covering media and selected stakeholders are conducted to disseminate information to specific target audiences for guiding and shaping market expectations on inflation and economic growth. The monetary policy report is identified as the only publication that includes projections for inflation and economic growth towards the next 2–3-year period among the publications of central banks in future. Therefore, the projections should be more accurate and consistent with the actual numbers to build confident toward forward looking policies in line with the established initial requirements in adopting an inflation-targeting framework.

Further, regarding monetary policy communication, measuring the effectiveness of monetary policy communication has also been emphasized as a requirement to identify communication gaps and fill them with recommended strategies to ensure clear and effective communication to a broader audience. In this regard, feedback mechanisms and surveys should be conducted in regular frequency. Ensure the reaching of monetary policy communication to the public can be identified as a challenging task that involves communication across tailoring different religious and cultural regions with demographic and psychographic profiles. Clear and clarity of monetary communication to be developed with a tailored approach ensuring the timely reach of key messages in line with the language policy of the country.

In conclusion to the inflation in Sri Lanka under the inflation targeting monetary policy framework, inflation movements in SL are recorded below 10 percent except for the extreme two-year period from 2021 -2023, which has recorded the highest-ever inflation in Sri Lanka, which could manage below 70 percent. Before 2021, even with the monetary targeting framework, inflation was managed within a single-digit level, which has been identified as favorable for a developing country to encourage economic activity. After the enactment of CBA, an inflation-targeting monetary policy was adopted with a targeted level of 5 percent with 2 percent adjustment flexibility to the margins, called the Flexible Inflation Targeting (FIT) framework. After that, inflation in Sri Lanka is again reported in its usual path of around 5 percent in mid-single up to 2024 Q2, and inflation projection for the medium-term outlook is also within the targeted level as per the inflation fan chart which was a key feature under the inflation targeting framework. Inflation fan chart inclusion within the inflation targeting framework aims to shape and manage the market's inflation expectation to facilitate risk and uncertainty decision-making. Forward guidance introduced after the global financial crisis also intends to guide the market by promising to keep the interest rate lower through the extra expansionary monetary policy tool. A more specific version of forward guidance policies, Forward-looking policies are applied to inflation targeting monetary policy, Inflation targeting ensures the target level of 5 percent inflation to guide the market and inflation expectation in facilitating maximum utilization of resources and thereby to achieve domestic price stability and other medium-term objectives of the economy.

5. Results and Findings

5.1. Results of Diagnostic Tests

For this study, two series were considered to estimate the model and projection, considering the higher sample size available for CCPI, 2013=100, compared to the limited data available for the new series of CCPI 2021=100. Data in both series were tested to confirm the stationary level performing unit root test under augmented Dicky Fuller test covering criterion given. Accordingly, the basic primary test results are below for both series of CCPI = 2013 and 2021 base years, against the null hypothesis H0: CCPI has a unit root for both series.

Table 1. Results of unit root test.

Series | Test for Unit Roots @ 5% Significant level | Test Statistics | P value | Stationary @ |

CCPI, 2013=100 | Level | 0.0511 | 0.9603 | |

1st difference | -5.6256 | 0.0000 | Level 1 |

CCPI, 2021=100 | Level | 2.1976 | 0.9916 | |

1st difference | -2.1843 | 0.0302 | Level 1 |

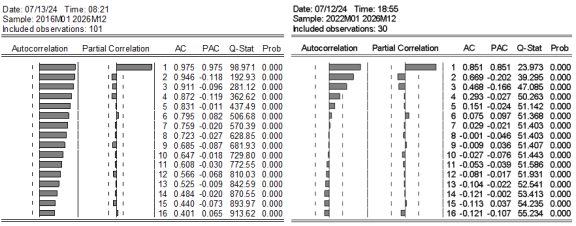

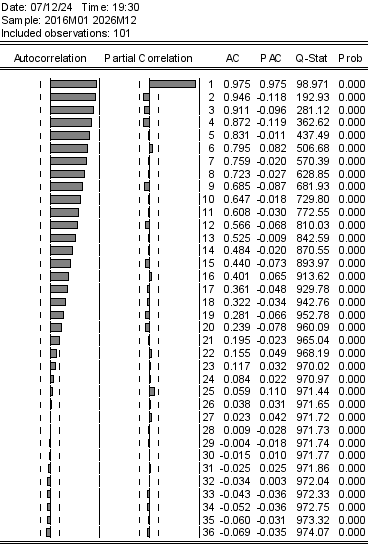

According to the unit root test results, Ho rejected the first difference of the test given the lower p-value than the 5 percent level. Therefore, both series were identified as stationary at the first difference, fulfilling the basis test of the stationary requirement for the data series. Then, the autocorrelation and partial autocorrelation checking are to be performed using correlograms, which might be helpful in detecting Autocorrelation, Moving Average, and the terms for AR(p, q) and MA(r, s) the impact of the current series.

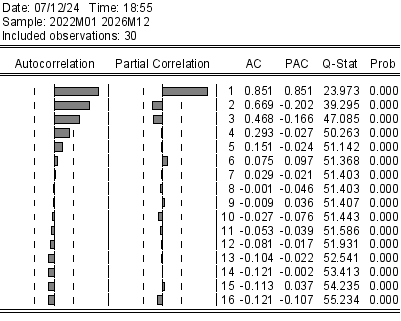

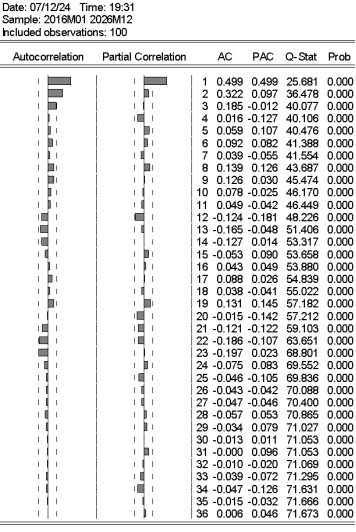

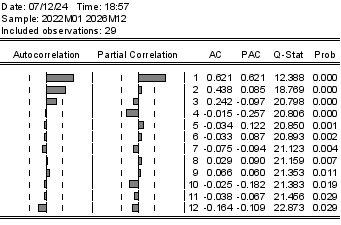

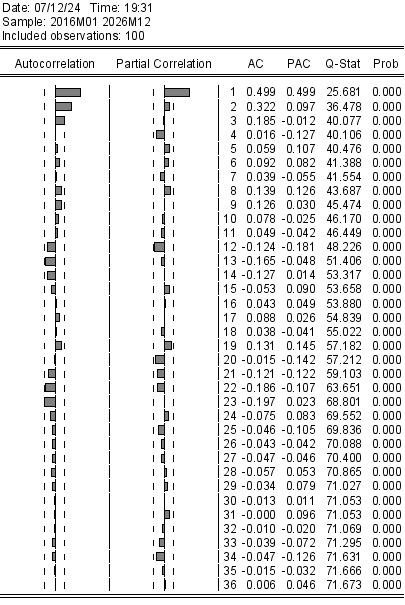

Figure 3. ACF and PACF functions of the CCPI 2013=100 and 2021=100.

As per the above correlograms, it can be observed the autocorrelation indicates for both series; further, the partial autocorrelation is detected only for the current series, and therefore, ARMA terms for CCPI 2021= 100 is determined as ARMA(1,0)(0,0) and ARMA term for CCPI 2013=100 as ARMA(3,2)(0,0). The next step is to run the model using appropriate criteria, which we use to determine the variable’s stationary at their first difference via the EViews software. As explained in the section discussing the methodology, Automatic ARIMA forecasting is employed to forecast inflation under inflation targeting, and the summary of the results are given below

Table 2. Summary of the Automatic ARIMA forecasting.

CCPI | Selected Dependent Variable | Model Max (AR, MA) Max Difference (SAR, SMA) | Number of ARMA Models estimated | Selected ARMA Model | AIC Value | SIC | HQC |

CCPI, 2013=100 | D(CCPI_2013) | (4,4)2(0,0) | 25 | (3,2)(0,0) | 5.5481 | 5.7305 | 5.6219 |

CCPI 2021=100 | D(CCPI_2021) | (4,4)2(0,0) | 25 | (1,0)(0,0) | 5.7175 | 5.8589 | 5.7180 |

Summary results first show that the selected models for both series are within the criteria we determined using ACF and PACF in correlograms. The first difference of the series was used to ensure its stationarity as a dependent variable. As per ARIMA specifications, the maximum criterion for the models is ARMA (4,4), Max difference (2), and seasonality adjustment for AR and MA is (0,0), which are within the specification determined using ACF, PACF, and unit root tests. The best model was selected by estimating 25 models for each series, which would be challenging to estimate manually. Information criteria which guide model selection, AIC and Bayesian Information criteria (SIC and HIC) are reported as the lowest for the selected two models. In addition, comparison to the two models estimated employing data for two base years CCPI 2013=100 and CCPI 2021=100, the projections are moving to the same directions with estimating higher index number for CCPI 2013=100 compared to CCPI 2021=100 data series. Compared to actual values, forecasting inflation using CCPI 2013=100 support for projections with lower increase of prices compared to the steeper projections for CCPI 2021=100. This could be a reason due to large sample size for n=100 compared to recent CCPI 2021=100 sample size for n=30 reflecting the consistency of the estimates. Accordingly, the forecasting will move under flexible inflation targeting framework, with 5% per cent plus 2% percent margin for both side fluctuations with CCPI 2013=100 model. Further, projections under CCPI 2021=100 model indicate more upwards movements of inflation in the latter part of 2025. Anyway, assessments of risk factors and judgements are also playing a vital role for inflation forecasting under the inflation targeting framework in conducting monetary policy. The indication of inflation movement within the 5 per cent target is reflected in both estimates for the forecasting length and near-term inflation should be adjusted with upside, downside risk and uncertainty factors. The results of the inflation projection are consistent with the primary test performed and determined. Therefore, the results of the CCPI and inflation projection are discussed to determine whether the projection is supported by the inflation-targeted level going forward.

5.2. Interpreting the Selected Automatic ARIMA Forecasting Models

Based on the results of diagnostic tests, summary of automatic ARIMA forecasting models, the two selected models are discussed for CCPI 2013 =100 and CCPI 2021=100 separately with necessary comparisons.

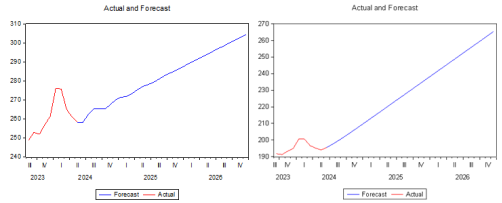

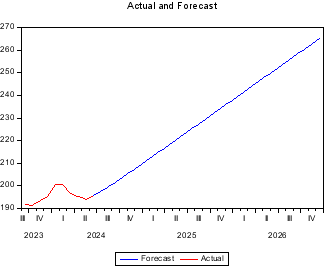

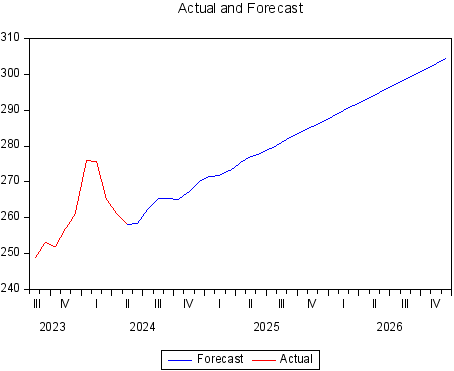

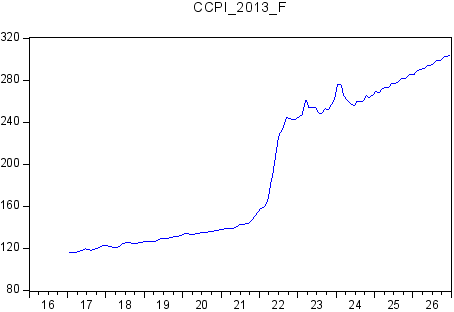

Figure 4. CCPI Actual and forecast for base year 2013 and 2021.

CCPI actual and forecast for both series indicate an increase of the index towards 300 points for CCPI 2013=100 and an increase towards 260 index points for CCPI 2012=100, spanning the 30-forecasting length up to the 2026 year. Index points in CCPI 2013=100 are substantially higher compared to CCPI 2021=100 due to capturing an increase of elevated prices during the period after 2020. Based on the CCPI forecast, time and the rate of change in price indices for a given period can be projected as below.

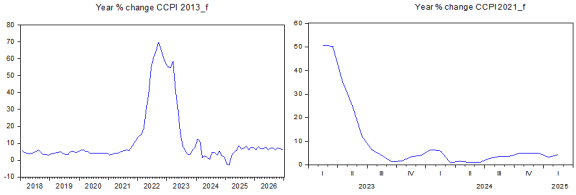

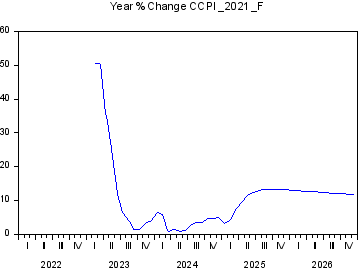

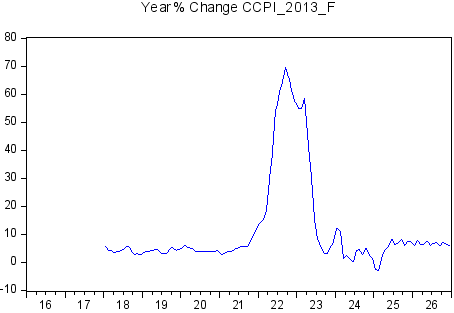

Figure 5. Inflation, Year% change of CCPI for 2013=100 and 2021=100.

According to the inflation projections based on the CCPI forecasting 2026, inflation indicates a managed level between 1-8 percent for the next two-year period, as per both series. As per the data employed for recent base year CCPI 2021=100, inflation would be more accelerated from the targeted level of 5 percent, which could be justified using reasons for the upside risk of inflation. Further, this could be a reason for reflecting more volatility for the CCPI 2021=100 series owing to limited data and consecutive months of deceleration of inflation after 2023. In addition, key monetary policy tools are used to conduct monetary policy and manage market liquidity which monitor under the active market operations on short term and long term basis. Money market interest rates that determined daily basis are facilitated to manage within the policy interest rate corridor as per the decision of market operation committee and the results of the daily money market operations are published in corporate website.

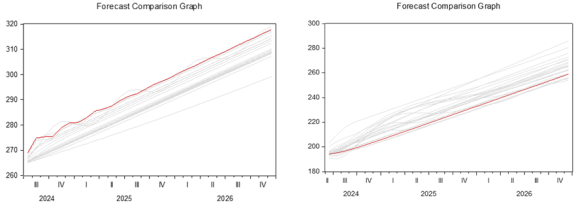

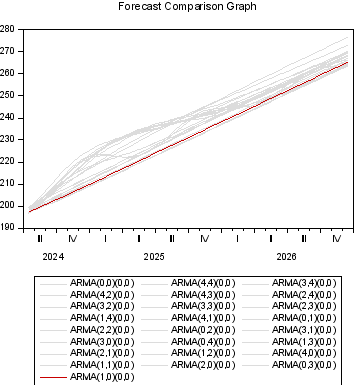

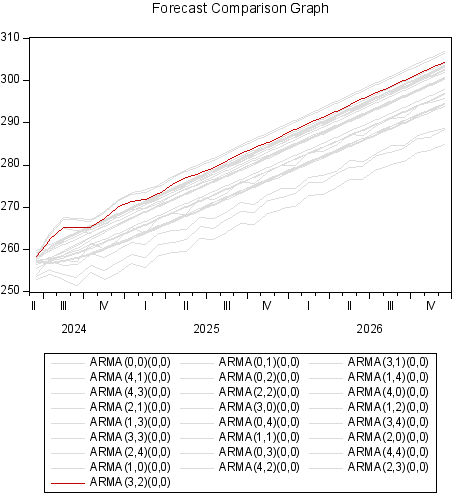

Forecast comparison is vital in justifying the selected model with the estimated number of forecasts. Accordingly, forecast comparisons for 25 model runs for each series are shown below.

Figure 6. Forecast comparison for CCPI 2013 = 100, and 2021 = 100.

As per the above forecast comparison for two series and 25 forecasts for each series, the selected criterion for models CCPI 2013=100, ARMA (3,2)2(0,0) is within the 25 forecast lines estimated and somewhat above the middle of the lines. It is not the top line of the forecast graph; therefore, considering the other criterion, the Automatic ARIMA forecasting is within the upper forecasting lines. Compared to that, the forecast for CCPI 2021=100 is not even in the middle but at lower borders in the forecast comparison graph. Therefore, model selection is used that indicates via the lowest AIC and Bayesian information criteria to confirm whether the best model is selected for CCPI forecasting during the period.

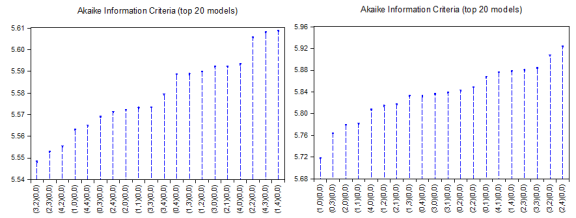

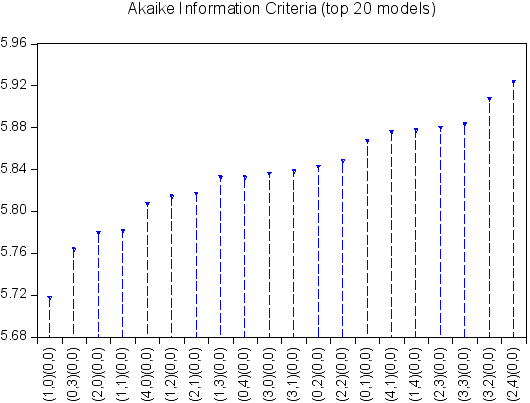

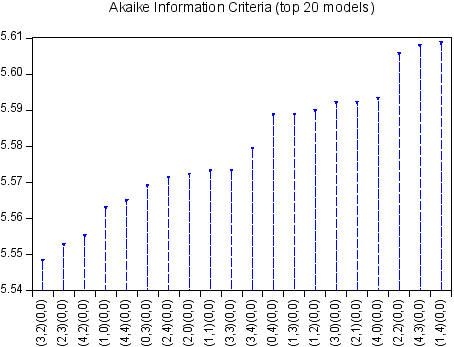

Figure 7. Akaike Information Criteria for top 20 models for CCPI 2013=100 and CCPI 2021=100.

According to the AIC model selection criterion, the best model indicates the lowest AIC for the selected top 20 models out of 25 models estimated. It is clear that ARMA (3,2)(0,0) gives the lowest AIC for CCPI 2013=100, and ARMA(1,0)(0,0) indicates the lowest AIC for other series. Further, SIC and HQI also in the same lower range as explained in the results summary above for both series. Therefore, the selected two models are identified as the best selected models as shown in the above charts.

5.3. Inflation Realized and Projections with Targeted Level of 5%

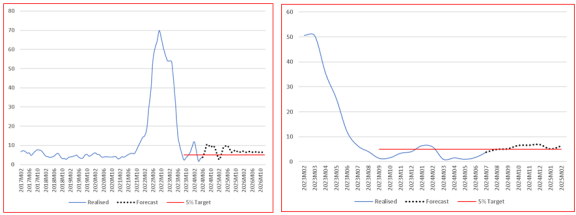

Inflation projections are given under the inflation targeting framework using an inflation fan chart that combines realized inflation and inflation projections with a probability of moving it up and down due to risk and uncertainties. According to the inflation realized and projected using CCPI for both series, targeted inflation level of 5 percent can be exhibited into a combined graph as given the figure below.

Figure 8. Inflation was realized, forested with a 5% targeted level for CCPI 2013=100, 2021=100.

The above figures show the inflation level realized up to 2024M06. Forecasting for the rest of the period with the targeted level of 5 percent for both series of CCPI was developed considering the forecasting data estimated under the above two models employing Automatic ARIMA models for CCPI 2013=100, ARIMA (3,2) 1(0,0) and for CCPI 2021=100 estimated model ARIMA (1,0)1(0,0) and with the targeted level of 5 percent into one graph which makes easy to understand given data in the past, targeted level and estimated data in futuristic approach which may helpful in guiding the decision-making process. According to the inflation realized projections under the 5 percent targeted level, inflation during the forecasting period will move below 8 percent and above 1 percent as upper and lower margins, respectively. Further, as per the Flexible Inflation Targeting (FIT) Framework, inflation target of 5 percent will fluctuate around 2 percent for both margins. Compared to the FIT framework, the projected inflation will also fluctuate around the target level, with the flexible margin of 2 percent deviating slightly in a few instances. Decision on key policy interest rates and daily open market operations will facilitate to manage the market interest rates and thereby achieve the domestic price stability. Further, given the independence as per CBA, limiting the fiscal dominance of the decision making body of the CBSL ensures the independence in making policy decisions while more accountable for policies to the Parliament and public which ultimately resonate for credibility. Risk factors that could lead to moving the inflation projections from the expected level are associated with the price of imported goods and energy, adverse weather conditions on agriculture production, wage pressure and exchange rate depreciation compared to the projected level as upward risk factors. At the same time, supply-side improvements and diminished purchasing power of consumers are identified as factors for downward adjustments of inflation from the target level. However, the uncertainty impact of political and other factors are also risk factors that should be considered carefully which could be a factor for demand full inflation.

Concluding the result interpretation, the estimated two models were selected in line with inflation forecasting models employed under empirical literature for one variable estimation techniques in econometrics. Considering the limited sample for the recently revised CCPI 2021=100 data series, two series were estimated for better comparison with confidence to guide future decision-making. Anyway, the results of both series are aligned without deviating from the targeted level of 5 percent and 2 percent lower and upper margins set under the Flexible Inflation Targeting (FIT) framework. Basic tests were performed to check the stationary level, autocorrelation, and partial autocorrelation. Accordingly, data series were identified as stationary at first difference. AR and MA terms were determined based on the ACF and PACF functions. Forecasting models were estimated using Automatic ARIMA forecasting techniques available in EViews. Two models with the exact specifications that we determined by performing basic diagnostic tests were estimated using Automatic ARIMA forecasting for the first difference of variable with ARMA (3,2)(0,0) for CCPI 2013=100, and ARMA (1,0)(0,0) for CCPI 2021=100. Forecast comparison in automatic ARIMA estimation techniques has been performed considering a maximum number of 25 models for each series, and the forecasted two models are within the upper and lower margins of the forecast comparison graphs. Further, the lowest AIC, BIC and HQI indicates the best model selected out of the top 20 models in the estimation process. Since we refer to the inflation forecasting model under the inflation targeting framework in conducting monetary policy, the information on inflation realized, projections and with 5 percent targeted level were combined into one graph, facilitating better visualizing all in one chart similar to the content under the inflation fan chart. Accordingly, inflation in both series indicates fluctuations between 1-8 percent as per estimated secondary sourced data employed for forecasting horizon of 30 months. This implies that inflation forecasting in this paper aligns with the flexible inflation targeting framework introduced recently to guide the market with forward looking monetary policy.

6. Conclusion and Recommendation

Inflation has been a popular topic under the macroeconomic variables. With this, inflation and flexible inflation targeting have been used as a framework for central banks to conduct monetary policy. New Zealand was named the first country to implement inflation targeting monetary policy in 1998. IMF has pointed out four initial conditions to ensure the successful implementation of the inflation targeting framework. Further, it describes countries that can implement inflation-targeting framework even while adhering to a few requirements instead of all four requirements, depending on the country’s economic and financial market condition. The Central Bank of Sri Lanka also adopted an inflation-targeting framework in conducting monetary policy with the enactment of No. 16 of the 2023 Central Bank of Sri Lanka Act in pursuing its primary objective, archiving and maintaining domestic price stability. A clear mandate has been provided to adopt inflation targeting while signing an agreement jointly with the government to set inflation targets and margin for flexibility. In case of a missed target for two consecutive quarters, a report should be submitted to the parliament through the Ministry of Finance. Further, this report should be made available to the public, also reflecting accountability of the central bank policies to the public, which may be a path towards a credible central bank. This paper aims to explain the literature, the new inflation targeting framework adopted by CBSL recently, and the inflation forecasting model under flexible inflation targeting considering the importance of inflation forecasting and updates to guide the market and shape inflation expectation to facilitate better decision-making which ultimately impacts on minimizing inflation forecasting errors in the inflation expectation survey. Key features of inflation targeting monetary policy framework include a clear mandate articulating 5 percent target and the 2 percent margin for flexible inflation targeting to achieve and maintain domestic price stability, the inclusion of an inflation fan chart for monetary policy press releases, and the inflation press release with recent updates on inflation projections to guide the market in facilitating better decision making. Furthermore, the monetary policy reports are to be published in line with the advanced released calendar given in the official website. Further, monetary policy reports should explain the rationale for arriving at the monetary policy decisions with macroeconomic, external sector, and other development of economic activities. Further, to facilitate forward-looking monetary policy, the outlook for inflation and economic growth should be published with an explanation of the possible risk of deviating from the projections. Communication was also identified as an effective policy tool for implementing inflation-targeting monetary policy framework to disseminate information on policy decisions to the stakeholders and a more comprehensive range of audiences with clear and straightforward language to ensure timely information and the minimum shock to the market.

As per empirical literature, the desired level of inflation for a developed country is given as 2 percent and 5 percent for a developing country. This desired level of 5 percent inflation has moved with more fluctuations for developing countries compared to 2 or below-desired level inflation for developing countries with fewer fluctuations. The impact of inflation on oil prices and imports was examined due to many open economies relying on this as essential imports. Accordingly, import prices are a factor that impacts inflation, which depends on including imported goods and services in the consumer basket. Among the other factors, the stock of money and money supply have been identified as a major factor that fluctuating inflation in developing countries. Demand-side factors have been influencing inflation in the short run in many countries under different time periods, identifying inflation as the number one enemy for an economy. Several studies concluded that inflation targeting helps to manage inflation within a given level of volatility, which may be useful to encourage economic activities for developing countries and ensure the confidence of price level increases within a range set to the projections. Under the monetary policy communication tool, inflation targeting plays a vital role in disseminating the recent and growth projections to the stakeholders and a wider range of audiences to facilitate decision-making and shaping inflation expectations. However, monetary policy transmission mechanisms and channels are also crucial for policy effectiveness. The impact of inflation on other variables has been examined using multivariate time series data analysis techniques, initiating regression analysis towards VAR and VECM modules, following basic diagnostic tests, and other tests to check the consistency of the estimated module. Single variable model analysis techniques have been employed for inflation forecasting, and other models were introduced after 1970. Autoregression Moving Average (ARMA) and Autoregression Integrated Moving Average (ARIMA) were popular modules in the empirical literature. At the same time, monetary authorities might use comprehensive analytical techniques to facilitate policy forecasts that capture risk and uncertainty with different scenarios. In this study, the Automatic ARIMA forecasting technique was used to forecast inflation considering the forecasting length as 30 months, using CCPI 2013=100, 2021=100 secondary sourced data for two base years due to limited data availability for recent CCPI 2021=100 series. Data for CCPI 2013=100 was considered from 2016 avoiding, an election year data in 2015 and with sufficient number of over 100 observations. Data for the two series were identified as stationary at the first difference, while autocorrelation and AR and MA terms were identified using ACF and PACF functions. The models were estimated using the Automatic ARIMA forecasting method using EViews software, providing the best analysis out of 25 estimations.

Accordingly, the selected models for inflation forecasting are ARIMA (3,2)1(0,0) for CCPI 2013=100 and ARIMA (1,0)1(0,0) for CCPI 2021=100 series. As per forecast comparison, the selected two modules are within the forecasting modules of each series, indicating the lowest AIC, SIC and HQC criteria for selecting the best model among the number of modules considered. According to the selected models, inflation projections for 30 forecasting lengths will be moved within 1 to 8 percent of flexibility around the 5 percent target level. As per flexible inflation targeting set in conducting monetary policy. Therefore, 5 percent inflation target with 2 percent up and down margins are within the inflation forecasting module estimated by the study. Therefore, the estimated forecasting results are within the FIT, in which the margin is widened as 3 percent for up and down volatility, which may result in risk and uncertainty. The reach of the lower and upper band of the margin will be in a few instances as per forecasting figures illustrated in the analysis of the results. Even with the recent unfavorable experience regarding inflation in Sri Lanka, the inflation path within the FIT for the next 2-year period has been indicated to build market confidence on inflation and interest rate. The indication of this inflation forecasting figure of around 5 percent could be a reason for the inflation movements in Sri Lanka for more than a decade, which have been recorded as a single-digit level except for the elevated inflation reported in the last two years. The estimated models indicate that it aligns with the inflation-targeting monetary policy framework to guide the market and inflation expectations. The results estimated using CCPI 2013=100 are consistent with the inflation forecasting module employed by the author (Rohini, 2023)

| [25] | Liyanage, D. R. "Inflation forecasting using automatic ARIMA model in Sri Lanka." International Journal of Economic Behavior and Organization 11.2 (2023). |

[25]

. This paper incorporated the inflation forecasting within the inflation targeting monetary policy framework employing updated data series under CCPI 2021 =100 for the new base year. Further, inflation projection can be deviate from the estimated level due to changes in upside and downside risk factors that depend on aggregate impact on the margins. As per evidence in the empirical literature, Inflation targeting is effective for managing inflation within a target level, which indicates the same for this study. As per empirical literature, inflation targeting does not guarantee for higher economic growth which has reported as marginal growth after the GFC in developed countries due to weaken relationship between variables.

Recommendations can be made since the inflation forecasting estimated in this study is consistent with the empirical literature and the flexible inflation targeting framework signed for the next two years. Inflation for the next 1–2-year period will be around 5 percent target. Further, these projections can be compared with monthly updated realized inflation data and the new projection, which will be available with quarterly updates to facilitate continuous guidance to the market. In line with the inflation movements around the target level of 5 percent, other macroeconomic variables will also be developed favorably toward economic growth. The interest rate will decline further with FIT and in line with the expected downward adjustment from commercial banks for already relaxed monetary policy measures adopted from Q2 2023. As per the CBA and the agreement signed for FIT with the government, the central bank is more accountable for its policies to the public. With that confidence, we expect that limited demand side factors will impact inflation due to the absence of fiscal dominance in monetary policy with the enactment of CBA, diminished consumer demand, and lower disposable income after the elevated inflation experienced recently. Therefore, income generation activities will be initiated with targeted 5 percent inflation and lower interest rates. Further capital buffers to ensure the resilience of the commercial banks to the various risks could be raised via issuing medium-term capital market investment instruments, which will also help to ensure financial stability. Credit demand and the effectiveness of monetary policy transmission mechanisms are also expected to be improved with more accountable policies—credit expansion for targeted sectors to be encouraged subject to the risk management frameworks of banks. Decision-making for new initiatives in economic activities relating to agriculture, industry, and services sectors can be implemented under the lower interest rate with targeted inflation, which is favorable for recovering production process, economic growth, and other medium-term objectives, achieving and maintaining domestic price stability. Export-oriented production initiatives are recommended to be increased with lower interest rate-supported funding facilitation to small and medium enterprises towards the other sectors of the economy, which will enhance the capital inflows to the country. Further, diversification of the economic activities which have been concentrated in the service sector can also be initiated and supported by required funding from the banks at lower interest rates or lower interest rates guaranteed by the government to achieve stability of the economic growth subject to external sector performance in line with inflation targeting monetary policy implementation measures. In addition, policies for strengthening external sector performance of the economy will be the utmost important to ensure the stability of the external sector due to Sri Lanka is in the process of debt restructuring negotiations and commencements of debt repayments after the negotiations in future. In that context, prioritized actions should be implemented to ensure healthy foreign exchange inflows compared to foreign exchange outflows of the country. Further, lower inflation under the 5 percent targeted policy outlook encourages the identification, initiation, and implementation of a medium-term robust and workable policy framework with the support of the monetary and fiscal sectors for sustained economic growth and the well-being of the society.

Abbreviations

GDP | Gross Domestic Product |

CBSL | Central Bank of Sri Lanka |

CBA | Central Bank Act |

GFC | Great Financial Crisis |

CCPI | Colombo Consumer Price Index |

DCS | Department of Census and Statistics |

ACF | AutoCorrelation Function |

PACF | Partial AutoCorrelation Function |

ARMA | AutoRegressive Moving Average |

ARIMA | AutoRegressive Integrated Moving Average |

AIC | Akaike Information Criterion |

SIC | Schwarz Information Criterion |

HQC | Hannin-Quinn Criterion |

SL | Sri Lanka |

MPR | Monetary Policy Review |

IT | Inflation Targeting |

FIT | Flexible Inflation Targeting |

Conflicts of Interest

The author declares no conflicts of interest.

Appendix

Summary of unit root tests.

Table A1. Unit root test a).

Null Hypothesis: CCPI_2013 has a unit root |

Exogenous: Constant | | |

Lag Length: 1 (Automatic - based on SIC, maxlag=12) |

| | | t-Statistic | Prob.* |

Augmented Dickey-Fuller test statistic | 0.051104 | 0.9603 |

Test critical values: | 1% level | | -3.497727 | |

5% level | | -2.890926 | |

10% level | | -2.582514 | |

*MacKinnon (1996) one-sided p-values. | |

Augmented Dickey-Fuller Test Equation | |

Dependent Variable: D(CCPI_2013) | |

Method: Least Squares | | |

Date: 07/12/24 Time: 18:40 | |

Sample (adjusted): 2016M03 2024M05 | |

Included observations: 99 after adjustments |

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

CCPI_2013(-1) | 0.000382 | 0.007483 | 0.051104 | 0.9593 |

D(CCPI_2013(-1)) | 0.503206 | 0.090889 | 5.536482 | 0.0000 |

C | 0.675633 | 1.225338 | 0.551385 | 0.5827 |

R-squared | 0.252377 | Mean dependent var | 1.504161 |

Adjusted R-squared | 0.236802 | S. D. dependent var | 4.416575 |

S. E. of regression | 3.858374 | Akaike info criterion | 5.568203 |

Sum squared resid | 1429.157 | Schwarz criterion | 5.646843 |

Log-likelihood | -272.6261 | Hannan-Quinn criter. | 5.600021 |

F-statistic | 16.20349 | Durbin-Watson stat | 2.102778 |

Prob(F-statistic) | 0.000001 | | | |

Table A2. Unit root test b).

Null Hypothesis: D(CCPI_2013) has a unit root |

Exogenous: Constant | | |

Lag Length: 0 (Automatic - based on SIC, maxlag=12) |

| | | t-Statistic | Prob.* |

Augmented Dickey-Fuller test statistic | -5.625613 | 0.0000 |

Test critical values: | 1% level | | -3.497727 | |

5% level | | -2.890926 | |

10% level | | -2.582514 | |

*MacKinnon (1996) one-sided p-values. | |

Augmented Dickey-Fuller Test Equation | |

Dependent Variable: D(CCPI_2013,2) | |

Method: Least Squares | | |

Date: 07/12/24 Time: 18:41 | |

Sample (adjusted): 2016M03 2024M05 | |

Included observations: 99 after adjustments |

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

D(CCPI_2013(-1)) | -0.495754 | 0.088124 | -5.625613 | 0.0000 |

C | 0.734631 | 0.408552 | 1.798134 | 0.0753 |

R-squared | 0.246002 | Mean dependent var | -0.021939 |

Adjusted R-squared | 0.238229 | S. D. dependent var | 4.397923 |

S. E. of regression | 3.838486 | Akaike info criterion | 5.548028 |

Sum squared resid | 1429.196 | Schwarz criterion | 5.600455 |

Log likelihood | -272.6274 | Hannan-Quinn criter. | 5.569240 |

F-statistic | 31.64752 | Durbin-Watson stat | 2.104257 |

Prob(F-statistic) | 0.000000 | | | |

Table A3. Unit root test c).

Null Hypothesis: CCPI_2021 has a unit root |

Exogenous: None | | |

Lag Length: 0 (Automatic - based on SIC, maxlag=7) |

| | | t-Statistic | Prob.* |

Augmented Dickey-Fuller test statistic | 2.197628 | 0.9916 |

Test critical values: | 1% level | | -2.647120 | |

5% level | | -1.952910 | |

10% level | | -1.610011 | |

*MacKinnon (1996) one-sided p-values. | |

Augmented Dickey-Fuller Test Equation | |

Dependent Variable: D(CCPI_2021) | |

Method: Least Squares | | |

Date: 07/12/24 Time: 18:52 | |

Sample (adjusted): 2022M02 2024M06 | |

Included observations: 29 after adjustments |

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

CCPI_2021(-1) | 0.011378 | 0.005177 | 2.197628 | 0.0364 |